Anatomy of the gauntlet

May 29, 2026 · The Forven team

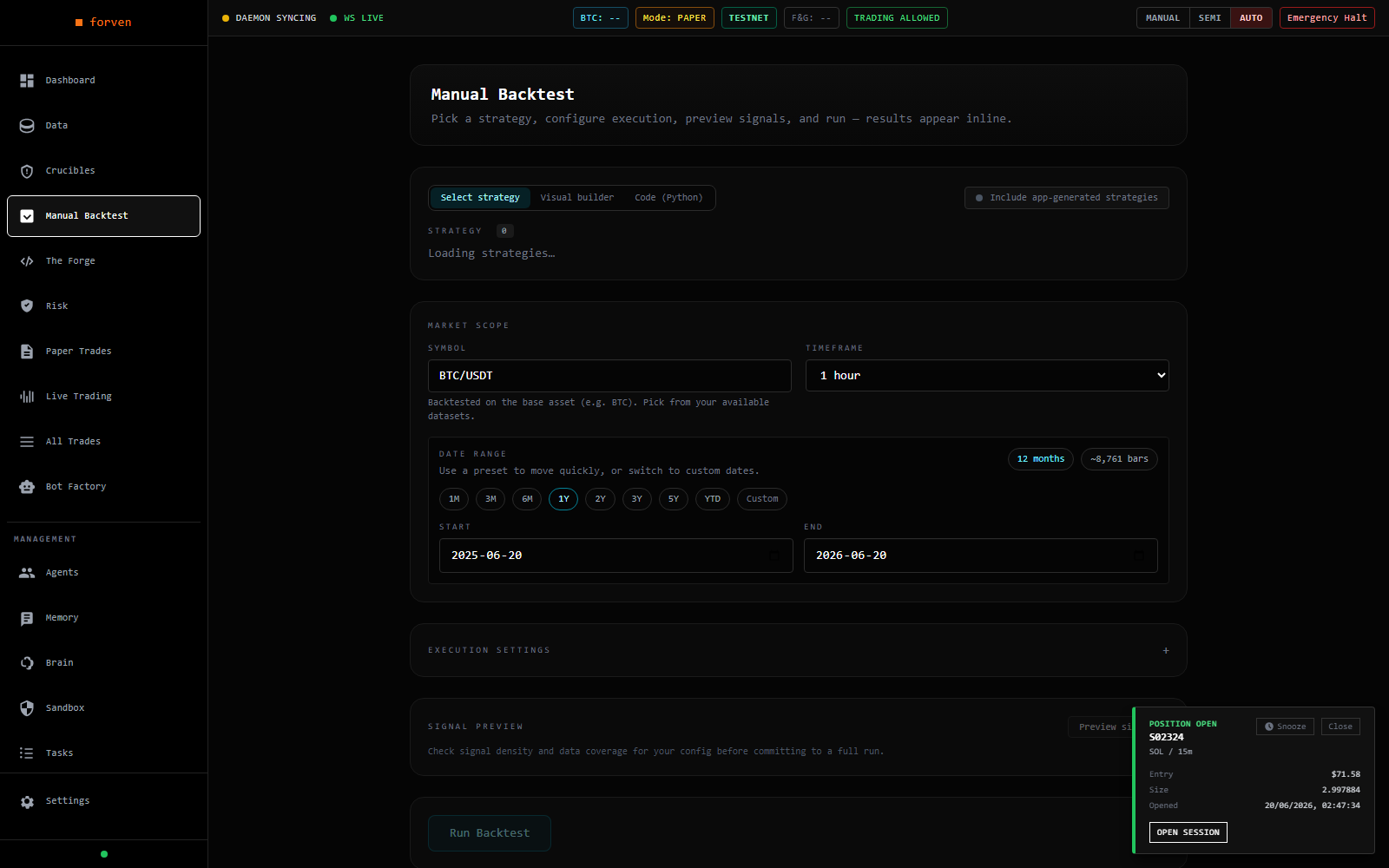

A single backtest, configured by hand. The gauntlet runs this same evaluation automatically, across many walk-forward windows the strategy has never seen. Illustrative; paper/testnet.

A strategy in Forven does not trade because you like it. It does not trade because the backtest curve goes up and to the right. It trades because it survived a sequence of tests it had never seen — and the moment it stops surviving, it stops trading.

Every strategy walks the same one-way road, and each stage exists to kill the strategy before the next one costs more. First compute, then time, then capital. Nothing reaches real money until it has cleared everything upstream. The full lifecycle lives in the pipeline; here is the shape of it:

researching → backtesting → quick_screen → gauntlet → paper → live_graduated → retiredA note on names before we go further. The marketing site uses simpler words than the engine does. Where the site says "screen," the engine means quick_screen. Where the site says "candidate," the engine means paper. We will use the engine's names, because those are what the UI and API actually report.

Before the gauntlet: the cheap triage

A strategy does not earn admission to the gauntlet by being interesting. It earns it by passing quick_screen — a fast triage over backtest metrics that rejects the two most common ways a backtest lies: overfitting and look-ahead leaks.

The guardrails are blunt on purpose. Out-of-sample profit factor under 1.05, fewer than 30 trades, an in-sample/out-of-sample Sharpe ratio above 3.0 — any one of these blocks admission. So does a Sharpe at or above 5.0, which on honest crypto data is not a triumph but the signature of accidentally reading tomorrow's price. The screen also refuses to alias in-sample data as out-of-sample: a strategy with no distinct unseen evidence has zero validation, not full validation.

This stage costs roughly five minutes. The next one costs real compute. That ordering is the whole philosophy — you only pay for a stage if you cleared the one before it.

Inside the gauntlet: five tests

Clear the screen and the strategy enters the gauntlet, an asynchronous battery that runs cheapest-first so weak strategies fail fast. First it sweeps timeframes, runs a parameter search, writes the best parameters back into the strategy, and re-validates them on fresh data. Then five tests run, each persisting a verdict before the next gate is even considered. Each stresses a different way an edge can be fake.

- Walk-forward analysis is the spine. The data is split into folds, each trained on the first portion and judged only on the portion it never saw. It answers the one question that matters: does the edge hold on unseen future data, or does it decay the moment tuning stops? The default bar is degradation no worse than 35 percent, with at least 40 percent of folds profitable. Drop walk-forward from the config and it self-heals on load, because without it the gauntlet has no honest signal at all.

- Cost stress doubles fees and slippage across the full window and measures how much survives. Many strategies that look fine on paper-thin margins die here, which is exactly the point. Live trading is not free.

- Monte-Carlo resamples the trade sequence to estimate tail risk, requiring most resamples to stay profitable and the 95th-percentile drawdown to stay bounded. It asks: how bad is the bad case, really?

- Regime split partitions trades by market regime — trending up, trending down, range-bound, high-volatility — and demands profitability in at least half of them. It catches the bull-market artifact that only works because the market only went one way.

- Parameter jitter perturbs the best parameters by a few percent and reruns the backtest dozens of times. If most survive, the parameters describe a real basin of edge rather than a single lucky coordinate balanced on a knife.

The default required set is walk-forward, parameter jitter, and cost stress; an empty required list forces all five. A genuine gate failure does not silently retry — a failed strategy is demoted back to quick_screen, and after three demotions it is redirected out of the tradable pipeline entirely, so a perpetual failure cannot loop forever burning compute.

Two gates, two philosophies

Surviving the battery is not the finish line. It earns an evaluation against the lean paper gate — and that gate, deliberately, is the easy one.

The design splits along a single idea: achievable paper, strict live. Paper costs nothing, so the paper gate asks only whether the strategy is obviously broken. Robustness score at least 50 out of 100, drawdown within bounds, out-of-sample profit factor at least 1.05. Reachable even in an ugly regime, so the funnel keeps moving. Clear it and the strategy trades against the live feed with simulated capital and zero risk.

One honest caveat that bears repeating: paper fills are local, carry no exchange order ID, and do not reconcile against any venue. Paper PnL is forward evidence of edge, not a profit forecast, and it is not a proxy for what live would do.

The gate from paper to live is the opposite animal — the hardest in the system, because it is the last one before real money. Fourteen days minimum in paper. At least fifty closed trades. A paper Sharpe that is really a per-trade t-statistic, not an annualized headline. And it does not take the gauntlet's earlier pass on trust — it re-runs the full robustness battery from scratch. Those numbers are eligibility thresholds, not predictions of return. Clearing them buys a small, capped allocation that ramps over weeks, watched the entire time by a decay kill-switch that auto-retires anything whose edge starts to rot.

Config can make any of these gates stricter. It can never make the capital gates looser — the floors are hard-coded, and there is no testing mode that opens a door to real money.

Why this exists

Most strategies fail the gauntlet. That is the design working, not the design failing. Every threshold on this path is a discipline mechanism, not a promise — Forven is a research tool, paper results are simulated, live results do not predict the future, and nothing here is financial advice. The gauntlet's job is narrow: make it hard for a fragile strategy to reach your capital. It cannot tell you a strategy that survives will profit. It can only make sure the ones that didn't survive never get the chance.

That is the entire bargain. A strategy earns the right to risk the next thing by surviving the last thing. If you want to watch it happen on your own ideas, the path starts by cloning Forven and running it.